Westside Observer

Westside Observer

February 2015 at www.WestsideObserver.com

Gambling With San Franciscoo Employees’ Retirement Fund

Looming Fiasco: Hedge Funds “Wealth Transfer”

Article in Print Printer-friendly PDF file

Westside Observer

February 2015 at www.WestsideObserver.com

Gambling

With San Franciscoo Employees’ Retirement Fund

Looming Fiasco:

Hedge Funds “Wealth Transfer”

by Patrick Monette-Shaw

Mayor Ed “Sharing Economy” Lee just proposed in his State-of-the-City speech sharing prosperity by tapping into City retiree funds for use in his down payment loan assistance program.

How benevolent of him. Retirees must be thrilled that he wants to “share” their pensions so untold recipients can obtain mortgages.

Despite recent warnings from billionaires Warren Buffett and George Soros against investing public employee pension money using hedge funds, some members of San Francisco’s Employees’ Retirement System (SFERS) board of directors and SFERS’ “chief investment officer” appear to know more than Buffett and Soros.

SFERS continues to

consider investing in hedge funds, after a state pension fund

(CalPERS), a Danish pension fund, and other prominent players

pulled out of their respective hedge-fund investments in recent

history.

SFERS continues to

consider investing in hedge funds, after a state pension fund

(CalPERS), a Danish pension fund, and other prominent players

pulled out of their respective hedge-fund investments in recent

history.

Apparently, some of SFERS Board members and staff think they are smarter than Soros and Buffett, and know more.

That’s why 81% of the City’s 23,000 City retirees who have a monthly pension of less than $2,500 (under $30,000 annually) rightly worry about investment decisions made on their behalf, without significant means to influence those investment decisions.

They have good reason to worry about decisions affecting their retirement income, since there are multiple plans to tap into the retirement fund, including a claim presented by Mayor Ed Lee during his State of the City speech on January 15 to tap $100 million from the retirement fund for a down payment loan assistance program that appears to be a premature claim, devoid of details.

Normally, investment advisors and trustees of public pension plans — such as the San Francisco Employees’ Retirement System (SFERS) Board of Directors — whose clients (beneficiaries of the pension fund) reject investment recommendations, have fiduciary obligations, and ethical and legal obligations, to back off.

SFERS Commissioners

are considering both various proposals to sink $3 billion or more

of the Pension Fund’s $20 billion portfolio into hedge funds,

and are being asked by the mayor to eventually consider allocating

$100 million to a new proposal to support his call to use the

retirees’ pension funds for questionable down payment loan

assistance programs administered by the troubled Mayor’s

Office of Housing.

SFERS Commissioners

are considering both various proposals to sink $3 billion or more

of the Pension Fund’s $20 billion portfolio into hedge funds,

and are being asked by the mayor to eventually consider allocating

$100 million to a new proposal to support his call to use the

retirees’ pension funds for questionable down payment loan

assistance programs administered by the troubled Mayor’s

Office of Housing.

Despite a resounding 2,300 signature petitions, e-mails, letters, phone calls, and public testimony from current and retired City employees objecting to investing in hedge funds that were submitted to SFERS’ Board members prior to its December 3, 2014 meeting, SFERS’ Board continues to consider investing in hedge funds that Plan beneficiaries strongly object to, ignoring their fiduciary duties to honor objections raised by their clients — the Plan’s beneficiaries.

Raiding San Francisco Retirees’ Cookie Jar

The smell of billions of dollars in municipal funds lures predators of every stripe seeking to get a slice of the pie. Particularly drawn to the smell of money are billionaires plotting to convert municipal assets into their incomes.

In the current case, a pot of $20.1 billion in the San Francisco Employees’ Retirement System (SFERS) pension fund is under assault. The lure of those billions draws strange bedfellows. SFERS’ pension fund is a tiny fraction of $2.6 trillion in public pension funds nationwide. The smell of trillions causes lots of rats to crawl out of the woodwork.

In January 2014,

SFERS lured Bill Coaker into returning to SFERS as its Chief Investment

Officer. Prior to returning to SFERS, Coaker was the senior managing

director of public equities in the University of California’s

Office of the Chief Investment Officer for just over six years,

earning $505,939 in 2013 helping manage the university’s

$90 billion pension, endowment, and campus assets portfolio.

In January 2014,

SFERS lured Bill Coaker into returning to SFERS as its Chief Investment

Officer. Prior to returning to SFERS, Coaker was the senior managing

director of public equities in the University of California’s

Office of the Chief Investment Officer for just over six years,

earning $505,939 in 2013 helping manage the university’s

$90 billion pension, endowment, and campus assets portfolio.

Many observers believe Coaker was lured back to SFERS in January 2014 for his so-called expertise with hedge funds and the “endowment model” of investing. A public records request revealed Coaker earned just $99,975 at SFERS between January and June 30, 2014; a second records request for data through December 31 is pending, but will probably reveal oaker earned approximately $200,000 during 2014. [Editor: See the February 14 Postscript #2 added at the end of this article after initially being posted on-line.]

Coaker’s Successor at UC Regents Undoing Coaker’s Portfolio?

Other observers now wonder whether UC Regents is in the process of undoing Coaker’s work during his tenure at the university. Randy Diamond reported on Pension and Investments On-Line on January 29, 2015 that the university’s new Chief Investment Officer, Jagdeep Singh Bachler has named Scott Chan as Coaker’s replacement as the university’s senior managing director of public equities. Chan will manage the university’s $30 billion public equities portfolio.

Notably, Diamond reports that Bachler has been engaged during his nine-month tenure as CIO in a major restructuring of the equities portfolio Coaker managed at UC Regents following Coaker’s departure in January 2014, reducing the number of external equities managers from 70 to 40 “because of concerns that the system was paying excessive fees and owned too many securities,” according to Mr. Bachler. Bachler didn’t comment on the equities portfolio’s performance under Coaker.

Who

Is Bill Coaker?

Who

Is Bill Coaker?

Coaker had formerly been a Senior Investment Officer at SFERS for just over two-and-a-half years between June 2005 and January 2008 managing SFERS’ “domestic and international emerging market” strategies before leaving for his six-year stint at the University of California. Prior to first joining SFERS in 2005, Coaker had been the Chief Investment Officer (CIO) at the Roman Catholic Diocese of Monterey for a stint of 13 years managing the Dioceses’ pension, endowment, and corporate assets programs.

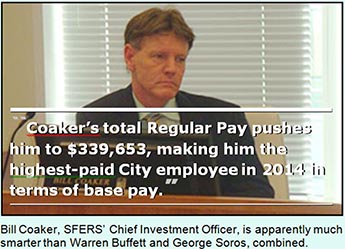

Why Coaker left the University of California and the Monterey Diocese to take a significant pay cut to be in charge of managing SFERS’ much smaller pension portfolio isn’t known, leaving observers wondering about a downward spiral in his career. Who would be willing to take a $300,000 pay cut — from $505,939 at UC Regents to just $339,653 at SFERS we just learned on February 10 — to manage SFERS’ pension portfolio that is one-quarter the size of the University of California’s Office of the CIO?

Coaker’s Linked-In profile indicates his focus at both the University of California and the Monterey Diocese was to implement the “endowment model of investing,” including investing in “absolute returns,” a financial industry “deconstruction” buzz word for hedge funds designed specifically to obscure the risky nature of hedge fund investments. His Linked-In profile also states that he recommended implementing an “endowment model” of investing at SFERS on his return in 2014.

Coaker’s

Various Hedge Fund Proposals

Coaker’s

Various Hedge Fund Proposals

So it was not much of a surprise that shortly after returning to SFERS in January 2014 Coaker submitted a proposal to SFERS’ Board of Directors in June to invest up to 15% — a cool $3 billion — of SFERS’ current Pension fund in hedge funds, drastically altering SFERS’ pension portfolio asset allocations. Coaker also presented “Mix 6B” on October 8, 2014 as an example of investing up to 36% — $7.2 billion — in hedge funds using an “endowment model” used by various private universities, illustrating the lunacy and weakness of industry-standard “optimizer” software that does not take into account public pension plans vs. private endowments, or the true risk of hedge funds and their illiquidity.

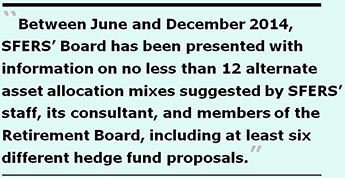

Between June and December 2014, SFERS’ Board has been presented with information on no less than 12 alternate asset allocation mixes suggested by SFERS’ staff, its consultant, and members of the Retirement Board, including at least six different hedge fund proposals.

Coaker’s various proposals have languished for almost a year without gaining approval from a majority of the Retirement Board to risk investing in hedge funds. And his various proposals have run into stiff opposition from Pension plan beneficiaries, the 54,823 current and retired City employees keenly interested in the health of their pension fund.

On June 1, Coaker first recommended allocating 15% to hedge funds. His proposal also ran into stiff opposition and intense scrutiny by one SFERS Board member. Although the agenda for SFERS’ December 3 meeting stated that the Board would again discuss Coaker’s recommendation to invest 15% in hedge funds, the Commissioners instead discussed — without adequate advance notice to members of the public and Pension plan beneficiaries — three alternate proposals that were not properly “noticed” on the agenda.

Two of the alternate

proposals were developed by SFERS’ Board president, Victor

Makras: One to allocate 3% to hedge funds, and a second proposal

to invest nothing (0%) in hedge funds. At the beginning of SFERS’

December 3, 2014 meeting, Commissioners were handed a third alternate

proposal dated the same date of the meeting (December 3) that

was reportedly developed by the trio of Makras, SFERS’ Executive

Director Jay Huish, and Coaker to invest 5% in hedge funds.

Two of the alternate

proposals were developed by SFERS’ Board president, Victor

Makras: One to allocate 3% to hedge funds, and a second proposal

to invest nothing (0%) in hedge funds. At the beginning of SFERS’

December 3, 2014 meeting, Commissioners were handed a third alternate

proposal dated the same date of the meeting (December 3) that

was reportedly developed by the trio of Makras, SFERS’ Executive

Director Jay Huish, and Coaker to invest 5% in hedge funds.

Across the various hedge fund proposals Coaker has presented, each of them anticipate a 6.5% return from any of the hedge fund investment proposals (whether investments in hedge funds of 3%, 5% or 15%).

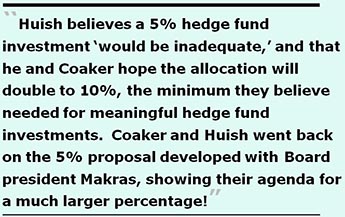

Plan beneficiaries believe the 5% hedge fund proposal is still too risky of an investment and lacks adequate transparency. The financial industry periodical Pension and Investments On-Line reported December 3 following SFERS’ meeting that Huish believes a 5% hedge fund investment “would be inadequate,” and that he and Coaker hope the allocation will double to 10%, the minimum they believe needed for meaningful hedge fund investments, if they prove they can successfully administer hedge funds.

On the very same day as the 5% proposal was introduced, Coaker and Huish went back on the 5% proposal developed with Board president Makras, showing their agenda for a much larger percentage! Huish asserted the 5% proposal would “be a good start,” signaling that once the door is opened to hedge fund allocations, the door will be kicked open to allow incremental increases to 10% or perhaps 15%, leaving Plan beneficiaries worried that Coaker will get what he wants, despite the warnings from billionaires Buffett and Soros that hedge funds are inappropriate for public pension plans.

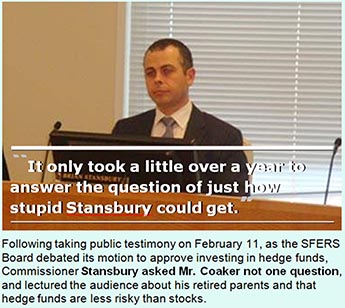

Notably, SFERS Board member Malia Cohen — the Board of Supervisor’s ex officio appointee to SFERS — is concerned SFERS’ Board may not have enough information regarding hedge fund investments. Tim Redmond’s web site, 48 Hills On-Line reported on December 3 following SFERS meeting that Cohen said “We have not had a solid conversation about our priorities and risks. I’m not going to articulate my position today.”

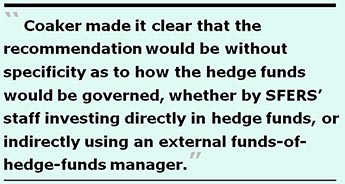

SFERS

Also Considering “Funds of Hedge Funds” Investments

SFERS

Also Considering “Funds of Hedge Funds” Investments

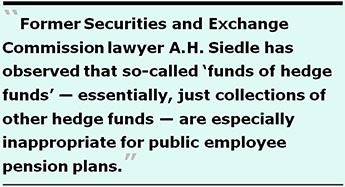

Pulitzer-prize winner Gretchen Morgenson wrote in “Slamming a Door on Hedge Funds” in the New York Times on September 20, 2014 that former Securities and Exchange Commission lawyer A.H. Siedle has observed so-called “funds of hedge funds” — essentially, just collections of other hedge funds — are especially inappropriate for public employee pension plans. Despite this, SFERS’ Board is considering investing in fund-of-hedge-funds. Funds-of-hedge-funds charge additional fees, and often duplicate investments in other hedge fund portfolios. Fund-of-hedge-funds have higher illiquidity (inability to quickly convert to cash or dispose of), with a minimum one-year lockup limiting the ability to get out quickly, and are less transparent than “direct” hedge funds.

Prior to December 3, none of SFERS’ staff and Angeles Investment Advisor’s proposals had rejected funds-of-hedge-funds as a viable investment opportunity. By report, SFERS’ staff favored direct hedge funds where Coaker would make the decisions directly. And these hedge funds would likely be approved by the Retirement Board in private closed sessions, without scrutiny from the public, or Plan beneficiaries.

But on December 3, SFERS Board members openly discussed using funds-of-hedge-funds. There was no discussion that funds-of-hedge-funds typically charge 3% in fees and 30% of profits on the investments, compared to the 2% in fees and 20% of profits charged by “direct” hedge funds.

The Board may be considering funds-of-hedge-funds because SFERS staff will reportedly then not be able to pick and choose which hedge funds to invest in — in part because of a lack of confidence in SFERS’ staff. This is simply a poor justification to use funds-of-hedge-funds.

Morgenson also reported in the September 20, 2014 New York Times that according to Preqin Ltd., a London research firm, hedge funds vastly underperformed the Standard and Poor’s (S&P) 500 stock index over the last one-, three-, and five-years, and lag on a 10-year basis, too. She reported fund-of-hedge-funds performance is even worse.

When Angeles Investment Advisors initially recommended that SFERS invest in hedge funds, Angeles failed to inform SFERS’ Board members that it concurrently runs a hedge fund operation out of the Cayman Islands, perhaps to avoid Security and Exchange Commission (SEC) scrutiny, as many hedge funds do. It turns out Angeles Investments’ hedge fund is a “fund-of-hedge-funds.”

In response to a records request placed with SFERS to obtain

correspondence received by SFERS opposing investments in hedge

funds and SFERS responses to the objections, of interest was an

e-mail SFERS Commissioner Herb Meiberger submitted to Huish and

Makras on October 24, 2014. Meiberger wrote:

Pension Funds Are Not Endowments

Pension Funds Are Not Endowments

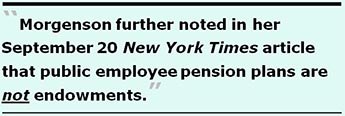

Morgenson further noted in her September 20 New York Times article that public employee pension plans are not endowments due to different cash-flow requirements, public pension funds are obligated to make regular payments to retirees, and unlike pension funds, endowments are more likely to have sophisticated staff to monitor investment managers.

If nothing else, the failure of SFERS staff to monitor its first foray in hedge fund investments in its so-called currency overlay program (see below) illustrates that SFERS’ staff has not demonstrated the skills and expertise required to monitor hedge fund investment managers.

Given the lack of due diligence with its currency overlay program, how can anyone believe SFERS staff’s due diligence monitoring hedge funds would be any different?

Disaslter

Waiting to Happen

Disaslter

Waiting to Happen

Information from Coaker’s Linked-In profile and a “Letter of Introduction” he submitted to SFERS’ Board and interested parties dated February 6, 2014 possibly in the first week after being re-hired — the latter of which contained a dash of Coaker’s hubris — paints a disaster waiting to happen with hedge fund investments.

First, Coaker’s Linked-In profile claims that as SFERS’ new Chief Investment Officer (CIO) he recommended SFERS should implement the “endowment model of investing.” There’s one small problem: A year after his arrival in January 2014, that model of investing has not been implemented as of January 2015 because it has faced SFERS Board member and Plan beneficiary’s opposition. Meet the emperor’s new clothes.

Apparently, Coaker skipped attending the class that taught that pension funds are not endowments, as he mistakenly brags on his Linked-In resume that he recommended implementing at SFERS.

He also claims that “absolute returns” — an interchangeable term for “hedge funds,” when hedge funds are getting bad media coverage — have a lower volatility, but most observers believe hedge funds are highly volatile, as many hedge funds have lost nearly 100% of their value.

Second, his Linked-In profile claims that his first gig as SFERS’ senior investment officer between June 2005 and January 2008, he had increased International and Emerging Markets Equity asset allocations in the first quarter of his employment, and over the two-and-a-half years of his first tenure between June 2005 and 2008, both international and emerging market stocks had outperformed the U.S. Equity market by 37% and 106% respectively.

But various data

from SFERS paint a very different picture, and some observers

disagree with Coaker whether international and emerging markets

had outperformed domestic equity shortly after he had fiddled

with asset allocations during his first stint at SFERS. First

of all, it takes time to fund various investment managers and

more time for investment results to materialize, so where Coaker

obtained data that his recommendations had performed better by

the end of 2008 is questionable, at best.

But various data

from SFERS paint a very different picture, and some observers

disagree with Coaker whether international and emerging markets

had outperformed domestic equity shortly after he had fiddled

with asset allocations during his first stint at SFERS. First

of all, it takes time to fund various investment managers and

more time for investment results to materialize, so where Coaker

obtained data that his recommendations had performed better by

the end of 2008 is questionable, at best.

According to SFERS’ consultant Angeles Investments, policy decisions that did not work so well for SFERS during Fiscal year 2009 (July 1, 2008 to June 30, 2009), included that “the international equity portfolio was a drag on [SFERS Plan] performance.” Angles also reported that “SFERS’ allocations to U.S. stocks [equity] benefited [overall Plan] performance.”

A Northern Trust analysis for the period ending June 30, 2009 showed that International Equity had a negative 33.23% return for the one-year period ending June 2009.

Second, in the five-year period between October 2009 and September 2014, one of SFERS’ emerging market managers, Mondrian and Wellington had the lowest five-year return of any of SFERS’ international stock managers. U.S. Equity managers did far better than International Equity, returning 15.6%. Also, for the five-year period ending September 30, 2014, SFERS’ bond portfolio returned 7.96% per year.

So during his first two-and-a-half-year job at SFERS, Coaker appears to have chosen to increase allocations to the poorest performing asset classes.

Coaker’s February 2014 “Letter of Introduction” starts off saying he is “humbled” to serve as SFERS’ Chief Investment Officer, and he hopes to serve with “class.” Do we need his hubris?

He goes on to state

that SFERS incurred a “peak-to-trough” decline of a

negative 32% during the FY 2008–2009 Great Recession. He

bemoans the fact that SFERS’ portfolio has not generated

“excess returns (meaning “alpha”) over the

past ten years, and SFERS’s total return has been completely

dependent on the beta exposure of its asset allocations.”

By chasing alpha, Coaker is again inviting hedge fund investment

disaster.

He goes on to state

that SFERS incurred a “peak-to-trough” decline of a

negative 32% during the FY 2008–2009 Great Recession. He

bemoans the fact that SFERS’ portfolio has not generated

“excess returns (meaning “alpha”) over the

past ten years, and SFERS’s total return has been completely

dependent on the beta exposure of its asset allocations.”

By chasing alpha, Coaker is again inviting hedge fund investment

disaster.

Chasing “alpha”

He asserts that SFERS needs to generate “attractive excess returns” (a.k.a., “alpha”) and that SFERS should “not be dependent on the markets to provide [SFERS] with good returns.”

Both alpha and beta are backwards-looking analyses of risk metrics, using calculations made with data that happened in the past, which obviously is no guarantee (or prediction) of future results. The excess return of an investment relative to return of the benchmark index used is a fund’s alpha. Alpha is the abnormal rate of return on an investment in excess of what would be predicted. Beta is a measure of the volatility, or risk, of an investment in comparison to the market as a whole.

His letter ends saying he planned to recommend changes in SFERS investment policies in 2014 that “should result in strong excess returns in the future.” [Editor: By “should,” Coaker means optimistically “might.”] It’s clear that Coaker believes he is better qualified to chase after excess alpha than Buffett or Soros.

What Coaker didn’t anticipate during 2014 was that billionaires Buffett and Soros would come along and recommend that public pension plans not invest in hedge funds at all.

Between June 2009 and June 2014, SFERS’ Pension Plan’s net assets grew from $11.9 billion to $20.1 billion — an increase of $8.2 billion — without needing to rely on, or chase, “excess alpha” returns. The $8.2 billion increase would have been $60 million higher, had SFERS not invested in a currency overlay hedge fund at the urging of SFERS’ “expert” Commissioner Joe Driscoll.

Of note, two recent articles illustrate why Coaker’s optimism of a 6.5% return on any hedge fund investments disregards industry experts. First, an article titled “Hedge Funds Really Did Underperform in 2014” on the Institutional Investors Alpha web site reported on December 29, 2014 that hedge funds had anemic average gains of the first 11 months in 2014 ranging from 2.85% to 4.61%, while the S&P 500 was up 11.9%.

Institutional Investors Alpha also reported on December 29 that the London-based research firm Preqin found that two-thirds of investors seek annualized returns of 4% to 6% from hedge funds. How Coaker expects to eke out a 6.5% return is one 800-pound gorilla. Institutional Investors Alpha says the other 800-pound gorilla in the room is a question of whether hedge fund fees are justifiable for lower returns, lower volatility, and less correlation. Institutional Investors Alpha conveniently neglected to note another 800-pound gorilla: Whether exorbitant hedge fund management fees are “justifiable” that billionaires Buffett and Soros warn against.

Institutional Investors Alpha also reported on January 27, 2015 that despite the “recent run of relatively lousy performance by some high-profile hedge fund managers and consistent underperformance among hedge funds in general since the end of the financial crisis of 2008,” hedge fund fees are falling, but not by much.

Second, Pension

and Investments On-Line reported on January 22, 2015 that hedge funds

saw tepid returns in 2014. A number of named hedge funds returns

for calendar year 2014 ranged from 2.5% to 4.5%, with one hedge

fund returning 6.1%. Pension and Investments On-Line reported

that “Broad hedge fund index returns were well below the

13.7% return of the S&P 500 in 2014 and also were significantly

lower than [returns for hedge funds in] prior years.” Why

Pension and Investments On-Line and Institutional Investors

Alpha reported different returns for the S&P 500 in 2014

is not known.

Second, Pension

and Investments On-Line reported on January 22, 2015 that hedge funds

saw tepid returns in 2014. A number of named hedge funds returns

for calendar year 2014 ranged from 2.5% to 4.5%, with one hedge

fund returning 6.1%. Pension and Investments On-Line reported

that “Broad hedge fund index returns were well below the

13.7% return of the S&P 500 in 2014 and also were significantly

lower than [returns for hedge funds in] prior years.” Why

Pension and Investments On-Line and Institutional Investors

Alpha reported different returns for the S&P 500 in 2014

is not known.

But what’s clear is that hedge funds performed poorly in 2014, and will probably perform poorly into the future, now that two major public employee pension funds — CalPERS and Dutch pension fund PensioenfondsZorg en Welzijn — have both pulled out of hedge fund investments. The trend to divest from hedge funds will likely snowball in 2015.

Two Billionaires Recommend Against Investing in Hedge Funds

On May 6, 2014 Warren Buffett advised SFERS Board member Herb Meiberger: “I would not go with hedge funds — would prefer index funds.”

As recently as Thursday, January 22, 2015, David Sirota reported in his International Business Times column that another towering figure in the financial industry — Soros Fund Management chairman, George Soros, who recently retired from his currency-focused hedge fund business — warned to “beware of investing retiree money in hedge funds,” during a session of the World Economic Forum in Davos, Switzerland (yes, the same Davos conferences that former Mayor Gavin Newsom is so fond of attending). “Soros cited management fees charged by hedge funds in arguing that steering billions of dollars of public employees’ money in such products is imprudent.”

Sirota reported that Soros noted that current market conditions are difficult for hedge funds. Despite the advice of two towering billionaire figures in the financial industry advising not to invest pension funds in hedge funds, rookie Chief Investment Officer Bill Coaker thinks he knows better than the two billionaires.

Apparently Coaker has the concurrence of rookie cop Brian Stansbury, rookie investor Joe Driscoll (who’s been woefully wrong before), and conflict-of-interest conflicted Wendy Paskin-Jordan, all SFERS Commissioners hoodwinked that they and Coaker know better than the two billionaire experts.

Recent Media Coverage

A whole host of recent media reports illustrate that the “emerging markets,” interest rate swaps, hedge funds, and other “derivative” high-risk investments preferred by Coaker and SFERS Commissioner Joe Driscoll have taken drastic downturns in the recent past.

CalPERS Just Opted Out of Hedge Funds; Why Would SFERS Opt In?

SFERS has made no

effort to reach out to ask CalPERS why on September 15, 2014 it

had opted out [pulled out] of its entire $4 billion investment

in hedge funds. CalPERS’ $4 billion hedge funds investments

represented a tiny 1.3% of its total $300 billion pension portfolio,

and cost it $135 million in fees annually. Why would SFERS opt

in, and go against the documented experience of others?

SFERS has made no

effort to reach out to ask CalPERS why on September 15, 2014 it

had opted out [pulled out] of its entire $4 billion investment

in hedge funds. CalPERS’ $4 billion hedge funds investments

represented a tiny 1.3% of its total $300 billion pension portfolio,

and cost it $135 million in fees annually. Why would SFERS opt

in, and go against the documented experience of others?

Remarkably, on September 29 Pension and Investments On-Line also reported that Michael Rosen, Chief Investment Officer and a principal at Angeles Investment Advisors LLC claimed that CalPERS’ rationale to divest its hedge funds investments was “not credible.” How could Rosen know this without discussing it with CalPERS?

Angeles Investment Advisors is SFERS’ current general consultant and may earn additional fees if SFERS invests in hedge funds. As such, Rosen may have a conflict of interest in driving SFERS to invest in hedge funds by bad-mouthing CalPERS.

CalPERS isn’t the only public pension to have divested from hedge funds in recent months.

Pensions and Investments On-Line reported on January 9, 2015, that the Dutch pension fund PensioenfondsZorg en Welzijn (PFZW’s ) eliminated its $5 billion hedge fund portfolio during 2014 because the hedge funds did not fully meet new investment criteria. Jan Willem van Oostveen, PFZW’s financial and investment policy manager said the “high cost” of investing in hedge funds “can only be justified if the returns are high.” He added that “with hedge funds, you’re certain of the high costs, but uncertain about the [rate of] return.”

Downturns in Alternative Investments

In September 2013, Matt Taibbi published “Looting the Pension Funds” for Rolling Stone magazine. He noted in relation to the Great Recession of 2008-2009 meltdown of the economy that:

More recently, the

New York Times reported on November 12, 2014 that some of

the world’s largest banks were fined $4.25 billion

for having conspired to manipulate foreign currency markets in

a currency-rigging scheme. Clearly, the currency overlay program

SFERS Commissioner Joe Driscoll had strongly advocated for in

2005 may have involved unsafe and unsound practices in the currency

trading by some of these same banks, including Barclays, which

withdrew from a settlement with the U.S. Justice Department due

to the bank’s concerns that the settlement would resolve

only a fraction of Barclay’s liabilities in the case.

More recently, the

New York Times reported on November 12, 2014 that some of

the world’s largest banks were fined $4.25 billion

for having conspired to manipulate foreign currency markets in

a currency-rigging scheme. Clearly, the currency overlay program

SFERS Commissioner Joe Driscoll had strongly advocated for in

2005 may have involved unsafe and unsound practices in the currency

trading by some of these same banks, including Barclays, which

withdrew from a settlement with the U.S. Justice Department due

to the bank’s concerns that the settlement would resolve

only a fraction of Barclay’s liabilities in the case.

On February 3, 2014 CNN Money reported that investors yanked more than $6.3 billion from emerging market equity funds the week before. Emerging markets refer to developing countries in Eastern Europe, Africa, the Middle East, Latin American, the Far East, and Asia. Investing in emerging markets — as Coaker advocates doing — is relatively high-risk.

When it comes to the interest-rate swaps SFERS’ Commissioner Driscoll had advocated investing in, readers should carefully read Matt Taibbi’s article “Everything Is Rigged: The Biggest-Price-Fixing Scandal Ever ” in Rolling Stone magazine’s April 25, 2013 issue. It details many of the world’s too-big-to-fail banks caught manipulating global interest rates.

Taibbi reports that

interest-rate swaps “are a tool used by big cities, major

corporations, and sovereign governments to manage their debt,”

and notes that interest-rate swaps were a $379 trillion

market in 2013. It’s an area ripe for corruption. Tabbi reports

the scheme to fix the prices of interest-rate swaps involve the

same banks, including Barclays and Bank of America. His reporting

is not to be missed.

Taibbi reports that

interest-rate swaps “are a tool used by big cities, major

corporations, and sovereign governments to manage their debt,”

and notes that interest-rate swaps were a $379 trillion

market in 2013. It’s an area ripe for corruption. Tabbi reports

the scheme to fix the prices of interest-rate swaps involve the

same banks, including Barclays and Bank of America. His reporting

is not to be missed.

SFERS’ Disastrous First Foray in Hedge Funds: “Currency Overlay”

SFERS’ staff’s previous failure to perform adequate “due diligence” on its so-called “currency overlay” program that lost upwards of $60 million was a complete disaster. Aware from meeting minutes and agendas of SFERS Board meetings that SFERS had completely terminated its failed currency overlay program, this author placed a records request to obtain any and all documents prepared by SFERS’ staff — not documents prepared by its highly-paid consultants — regarding due diligence of the currency overlay program performed by SFERS staff.

Wikipedia reports that currency overlay is a financial trading strategy conducted by specialist firms that manage the currency exposures of large clients. Currency overlay managers conduct foreign-exchange hedging on their clients’ behalf, selectively placing and removing hedges to achieve the objectives of the client. So-called currency overlay “pure alpha mandates” [asset allocations] are set up to allow the manager as much scope as possible to take speculative positions. As such, they are similar in nature to foreign-exchange hedge funds in terms of objective and trading style. Why would a public pension fund with long investment horizons do this?

L’Affaire

FX Concepts

L’Affaire

FX Concepts

A financial industry periodical, InstitutionalInvestor.com, reported on August 8, 2005 that SFERS Board member Joe Driscoll had prominently advanced and “pushed SFERS to become one of the first public pension plans to invest in ’emerging markets’,” including a $100 million investment in a fund investing mainly in sovereign debt instruments, including defaulted loans, and a second SFERS $75 million investment in 2002 in an emerging markets local-currency debt fund that held positions in interest rate swaps and other derivatives.

Finally, InstitutionalInvestor.com reported Driscoll had “pushed for [SFERS’] new currency overlay program that began July 1, [2005],” a program that relied heavily on hedge funds.

As an aside, SFERS’ Executive Director Jay Huish is currently using spin control to deconstruct whether the currency overlay program had involved using hedge funds, which of course it had, as documented in the New York Times, Institutional Investor on-Line, and other investigative journalism venues. Huish is clearly attempting to write revisionist history. Huish was referring to an outfit named FX Concepts, which only does hedge funds, as Reuters noted in 2013.

Comically, Huish denied during a media interview — posted on YouTube following the January 7 Board of Supervisors hearing to reappoint SFERS Commissioner Wendy Paskin-Jordan — that SFERS’ failed “currency overlay” program had not involved hedge funds. Of course it had, but Huish wants us to believe that “had” is the new definition of “had not,” a claim ludicrous because newspapers around the country had all acknowledged the currency overlay program was administered by a hedge fund manager. Huish creatively claimed the currency overlay program was a different “product line” of the manager and not hedge funds, but it appears the investment manager had a single line of business: Hedge funds.

Huish may be the only person on the planet who has not heard the old adage “If it looks like a duck, walks like a duck, swims like a duck, and quacks like a duck, then it’s a duck.” FX Concepts, one the world’s biggest currency hedge fund, once managed more than $14 billion in assets.

The currency overlay program initiated in 2005 was plagued with losses and high fees. On May 8, 2013, the SFERS Board voted to terminate the hedge fund managed by BlackRock because SFERS was its last client. SFERS’ staff and its consultant recommended re-allocating the $450 million investment to an outfit called FX Concepts. Five months later, FX Concepts declared bankruptcy.

One of SFERS’

currency overlay managers was Barclays Global Investments (BGI),

the same outfit that SFERS Board Member Wendy Paskin-Jordan is

currently embroiled in regarding her potential conflict-of-interest

status as a Trustee of various BGI money market funds, among other

problems.

One of SFERS’

currency overlay managers was Barclays Global Investments (BGI),

the same outfit that SFERS Board Member Wendy Paskin-Jordan is

currently embroiled in regarding her potential conflict-of-interest

status as a Trustee of various BGI money market funds, among other

problems.

In 2013, SFERS finally pulled out of its first hedge fund investment in its so-called “currency overlay” program. By January 2014, SFERS had completely eliminated its currency overlay program pushed by SFERS Commissioner Driscoll.

Missing Oversight and Due Diligence?

In response to a second records request, SFERS provided approximately 44 documents across two PDF files, with a total of 247 pages of material. Of them, fully 210 pages across 18 documents were authored by Leslie Kautz at Angeles Investment Advisors, a consultant to SFERS, documents which were not requested.

Of the remaining 26 documents totaling just 38 pages authored by SFERS staff, at least 16 pages were “agenda item” scheduling memo’s for SFERS’ various Board of Directors meetings, leaving a skimpy 22 pages of SFERS staff-authored so-called “due diligence” documents.

A professional familiar with the type of information typically contained in due diligence documents believes the documents prepared by SFERS’ staff do not amount to actual due diligence of the currency overlay program at all. Instead, they appear to more properly be some sort of documents administering the currency overlay programs, as opposed to formal due diligence analytical reports, since there were no reconciliation of investment statements and no analyses of investment transactions. Most of the staff documents simply regurgitated materials prepared by Angeles Investment Advisors.

The professional who reviewed the 247 pages concluded that in addition to the lack of reconciliation of investment statements and the lack of investment transaction analysis, the documents also do not show 1) SFERS’ Staff’s on-going due diligence; 2) Meetings with external investment managers; or 3) Discussions with external investment managers.

A third records request

seeking the dollar amount remaining in the currency overlay hedge

funds FX Concepts was managing at the time it was instructed on

September 13, 2013 to initiate the orderly liquidation of SFERS’

account, the date on which the “orderly transition”

liquidation was completed (i.e., the date on which FX Concepts

stopped any transactions on behalf of SFERS and returned any outstanding

balance to SFERS), and the dollar amount of any funds returned

to SFERS if any, resulted in a response from SFERS saying there

were “no responsive records” to the third records request.

A third records request

seeking the dollar amount remaining in the currency overlay hedge

funds FX Concepts was managing at the time it was instructed on

September 13, 2013 to initiate the orderly liquidation of SFERS’

account, the date on which the “orderly transition”

liquidation was completed (i.e., the date on which FX Concepts

stopped any transactions on behalf of SFERS and returned any outstanding

balance to SFERS), and the dollar amount of any funds returned

to SFERS if any, resulted in a response from SFERS saying there

were “no responsive records” to the third records request.

“No responsive records” translates to more evidence of the lack of due diligence. How could SFERS staff not have documentation of the date on which FX Concepts was finally and fully divested?

Addditional Lack of Due Diligence

A fourth records request provided the most damning evidence of the lack of due diligence performed by SFERS’ staff and the majority of its Board of Directors.

In response to this author’s January 11, 2015 fourth records request for any and all correspondence from SFERS Board Commissioners to SFERS staff regarding the staff’s due diligence of the currency overlay program between January 1, 2013 and January 2015, the records SFERS provided shows only one Commissioner — elected member Herb Meiberger — exercised fiduciary responsibility to perform due diligence of the currency overlay program.

That could be because Meiberger is a member of the Chartered Financial Analyst Institute, a designation that binds him to a code of ethics requiring due diligence from members of financial investment professionals. CFA members have an overarching duty to exercise reasonable care and prudent judgment for the benefit of their investment clients, and to place their clients’ interests above their employer’s or own interests.

The CFA’s code of ethics requires chartered analysts to exercise due diligence, independence, and thoroughness in analyzing investments, and making investment recommendations and investment actions. This should also apply to Commissioner Driscoll, who is also a member of the Chartered Financial Analyst Institute.

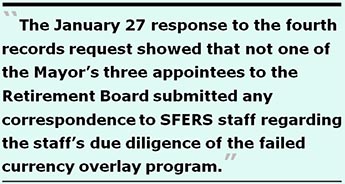

The January 27 response

to the fourth records request showed that not one of the Mayor’s

three appointees to the Retirement Board — Commissioners

Victor Makras, Wendy Paskin-Jordan, and Leona Bridges — submitted

any correspondence to SFERS staff regarding the staff’s due

diligence of the failed currency overlay program. Nor had the

other two elected Board members, Commissioners Stansbury and Driscoll,

submitted any correspondence to SFERS staff. Nor had sitting City

Supervisor Malia Cohen — the Board of Supervisor’s ex

officio appointee to SFERS’ Board — submitted any

correspondence to SFERS staff regarding SFERS’ staff’s

due diligence.

The January 27 response

to the fourth records request showed that not one of the Mayor’s

three appointees to the Retirement Board — Commissioners

Victor Makras, Wendy Paskin-Jordan, and Leona Bridges — submitted

any correspondence to SFERS staff regarding the staff’s due

diligence of the failed currency overlay program. Nor had the

other two elected Board members, Commissioners Stansbury and Driscoll,

submitted any correspondence to SFERS staff. Nor had sitting City

Supervisor Malia Cohen — the Board of Supervisor’s ex

officio appointee to SFERS’ Board — submitted any

correspondence to SFERS staff regarding SFERS’ staff’s

due diligence.

The January 27 response did uncover that as far back as November 2013, Commissioner Meiberger had requested from SFERS Executive Director Jay Huish, with a copy to Board president Victor Makras, information regarding adherence to SFERS’ policies, including due diligence issues.

Between November 2013 and March 6, 2014, SFERS Commissioner Meiberger was forced to place at least three separate public records requests — some of them multiple times, and one three times — to obtain information from SFERS’ staff (which records requests from SFERS staff went unanswered).

In a nutshell, it appears that several levels of due diligence were not performed by SFERS’ staff, SFERS’ general consultant (Angeles Investment Advisors), and the various external program managers involved. Multiple people failed to monitor the loss of key employees at the FX Concept currency overlay manager, and the loss of FX Concepts’ key clients.

When asked what aspect of investing in hedge funds he would you most want to educate SFERS Plan beneficiaries about — illiquidity, risk, volatility, transparency, or some other aspect — Meiberger said:

Who’s Wlatching SFERS’ Watch Lists?

Both the loss of key clients and key employees are grounds in SFERS’ formal Investment Policy Guidelines to have placed FX Concepts on SFERS’ “watch list,” but FX concepts was never put on SFERS’ watch list. As Meiberger’s December 2013 memo to Huish and Makras notes, both SFERS staff and its general consultants (Angeles) failed to place FX Concepts on SFERS’ watch list during each of the four quarters in 2012, and the first two quarters in 2013.

Had SFERS staff performed a simple Google search about FX Concepts, they would have found both a major loss of clients and loss of key employees two years before SFERS staff had inexplicably recommended in May 2013 awarding FX Concepts more pension funds to invest in the currency overlay hedge funds. SFERS staff failed to monitor the managers, or to put them on SFERS’ watch list.

In an eventual staff memo dated October 9, 2013, SFERS staff finally terminated FX Concepts due to an “emergency” and recommended that SFERS’ Board rubber-stamp the staff’s decision; the memo failed to note that key personnel had left FX Concepts long before the memo was written, and made no mention of the loss of key clients. An aiCIO.com article as early as March 20, 2012 noted there had been a “mass exodus” of FX Concepts employees. Another February 2013 aiCIO.com article reported the loss of two of FX Concepts’ key clients, leaving SFERS as FX Concepts’ last remaining institutional client, substantially increasing FX Concepts’ business risk and SFERS’ investment risk.

SFERS’ staff and Angeles Investment Advisors — who are both required by SFERS’ November 2012 Investment Policy and Guidelines to notify the SFERS Board of significant changes that may affect investments — failed to notify SFERS’ Board of either of FX Concepts’ loss of clients and staff.

Most appallingly,

SFERS’ staff and general consultant Angeles failed to even

notify SFERS’ Board of FX Concepts’ October 2013 bankruptcy.

Most appallingly,

SFERS’ staff and general consultant Angeles failed to even

notify SFERS’ Board of FX Concepts’ October 2013 bankruptcy.

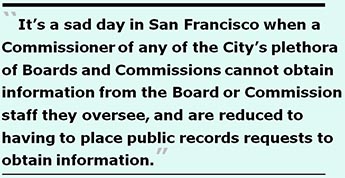

Meiberger noted in his December 2013 memo that SFERS’ Board has fiduciary responsibilities for pension fund oversight, and asked several questions about delegation of oversight of the currency overlay program and responsibility for the watch list, asking what evidence there may have been of SFERS’ staff’s oversight. Despite having placed multiple, formal Sunshine Ordinance records requests, Meiberger asserted in December 2013 that he had not received a single document produced by SFERS staff regarding oversight. He pointedly asked whether due diligence by SFERS staff was being performed on schedule.

It’s a sad day in San Francisco when a Commissioner of any of the City’s plethora of Boards and Commissions cannot obtain information from the Board or Commission staff they oversee, and are reduced to having to place public records requests to obtain information. It’s even sadder when they are forced to place a records request, and are then told there are no responsive records.

By January 2015, Mr. Huish had apparently never responded at all to a memo Meiberger had submitted 15 months earlier in November 2013. Huish, as the Retirement Board’s Executive Director, may be the only City commission director believing he can ignore responding to an inquiry from one of his own Commissioner’s for over a year.

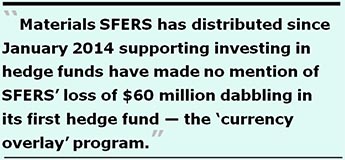

SFERS was Angeles Investment Advisor’s only client in currency overlay. SFERS’ staff and its consultant failed to perform adequate due diligence on either FX Concepts or the overall currency overlay program that Barclays Global Investors (BGI) was involved in. Materials SFERS has distributed since January 2014 supporting investing in hedge funds have made no mention of SFERS’ loss of $60 million dabbling in its first hedge fund — the “currency overlay” program.

The complete, multi-layered failure to perform due diligence on the currency overlay program and FX Concepts more than likely involves “nonfeasance” (failure to perform an act required by law) rather than simple “malfeasance” (malfeasance in office, often called official misconduct, is the commission of an unlawful act, done in an official capacity that affects the performance of official duties).

Pension Plan Members Speak: Public Testimony and On-line Survey Results

As noted at the beginning

of this article, trustees of public pension plans with fiduciary

obligations — such as SFERS’ Board of Directors —

whose clients reject investment recommendations have ethical and

legal obligations to back off. But despite over

2,300 e-mails, petition signatures, and public testimony presented

by Pension Fund beneficiaries over the last six months opposing

investing in hedge funds, SFERS’ Board and staff are charging

ahead anyway with hedge fund proposals, despite thoughtful objections

by Plan beneficiaries regarding how their contributions to the

Pension Plan will be invested.

As noted at the beginning

of this article, trustees of public pension plans with fiduciary

obligations — such as SFERS’ Board of Directors —

whose clients reject investment recommendations have ethical and

legal obligations to back off. But despite over

2,300 e-mails, petition signatures, and public testimony presented

by Pension Fund beneficiaries over the last six months opposing

investing in hedge funds, SFERS’ Board and staff are charging

ahead anyway with hedge fund proposals, despite thoughtful objections

by Plan beneficiaries regarding how their contributions to the

Pension Plan will be invested.

Prior to SFERS’ December 3 Board meeting, it was hoped that if the Board heard from at least 2,000 Pension Plan members that Commissioners might pay closer attention, and that opposition to investing in hedge funds would demonstrate greater validity. Following the December 3 Board meeting, ex officio Board member Supervisor Malia Cohen acknowledged that the 2,000+ signatures represent significant opposition to the various late-breaking hedge fund proposals submitted by SFERS staff and its consultant.

“Who Are You Trying to Kid?”

In addition to the 2,300 signature petitions submitted to SFERS between June and December 3, 2014 opposing investing in hedge funds, many current and retired City employees have presented thoughtful testimony at a series of SFERS Board meetings and in written correspondence. While all of the testimony and correspondence has been compelling, several prominent firefighters submitted thoughtful opposition.

Take for instance Elmer Carr, a retired Fire Department captain, who wrote to the Retirement Board on July 21, 2014 saying that the Board has an obligation to seek approval of their supervisors, meaning the retired and active members of the retirement system. He noted “We are watching and we are concerned,” about investing billions of SFERS portfolio into hedge funds.

Or take Joseph Soares, another retiree who recommended on September 6 investing in low-cost index funds, rather than hedge funds. He “considers anyone proposing that our pension money be handled by hedge funds, as totally irresponsible.”

Or take Kevin Callanan, another Fire Department retiree, who noted on September 7 that Bill Coaker may have “smoke and mirrored the unassuming Diocese of Monterey, but rest assured retired employees of [the City] will not stand for another carpet bagger raiding our [pension system].”

Or consider retired

Fire Department battalion chief John Murphy who noted on September

7 that there is a “storm of protest from pensioners”

regarding Coaker’s advice to invest 15% of SFERS’ conservatively-built

pension fund in a risky and expensive venture into hedge funds.

For his part, Bill O’Neil noted on October 1 that given CalPERS

is dropping its investments in hedge funds, he cannot understand

how SFERS’ Board is even considering putting money in such

financial instruments, and urged the SFERS Board not to include

hedge funds in the system’s portfolio.

Or consider retired

Fire Department battalion chief John Murphy who noted on September

7 that there is a “storm of protest from pensioners”

regarding Coaker’s advice to invest 15% of SFERS’ conservatively-built

pension fund in a risky and expensive venture into hedge funds.

For his part, Bill O’Neil noted on October 1 that given CalPERS

is dropping its investments in hedge funds, he cannot understand

how SFERS’ Board is even considering putting money in such

financial instruments, and urged the SFERS Board not to include

hedge funds in the system’s portfolio.

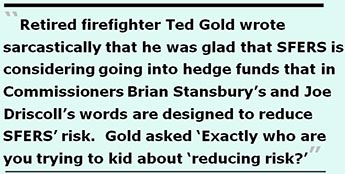

Finally, take retired firefighter Ted Gold, who noted to Huish and Coaker on November 1 that SFERS Commissioner Brian Stansbury had forwarded Elmer Carr a link to an article by Richard Baker on the Institutional Investors Alpha web site that advocated for using pension funds to invest in hedge funds. Gold noted that Stansbury and Baker had “cherry picked” a single positive article about hedge funds, ignoring a slew of seven articles on Institutional Investors Alpha that were negative about hedge funds and describe hedge fund losses of 2.5%, 3.45% and up to 12% during 2014.

Gold wrote sarcastically that he was glad that SFERS is considering going into hedge funds that in Commissioners Brian Stansbury’s and Joe Driscoll’s words are designed to reduce SFERS’ risk. Gold asked “Exactly who are you trying to kid about ’reducing risk?’,” before he recommended not investing in hedge funds.

On-Line Survey

When news surfaced that San Francisco’s International Federation of Technical and Professional Employees (IFTPE) Local 21 had formed an unnamed 12- to 15-member Hedge Fund Advisory Committee to weigh in on proposals to invest SFERS pension funds using hedge funds, Pension Plan beneficiaries became worried that Local 21 had wrongly concluded that only a “small number” of plan beneficiaries opposed investing in hedge funds. Local 21’s Advisory Committee ended up recommending investing up to 10% ($2 billion) of the pension portfolio in hedge funds, most likely contrary to its own members’ preferences.

So an individual with the pen name of “Publius Poplicola,” (Friend of the People), created three on-line survey instruments to gauge union members concerns about investing in hedge funds: One survey for Local 21 members; a slightly-differently worded survey for public safety employees, including police, firefighters, and sheriff employees; and a third survey for all other “miscellaneous unions,” which cover everybody else from secretaries to doctors, lawyers to librarians, nurses and certified nursing assistants to medical records technicians, etc.

[Editor: The pen name “Publius Poplicola” appears to have been modeled after the pseudonym “Publius” that was used by the authors of The Federalist Papers to publish their articles anonymously between October 1787 and August 1788.]

Results of the on-line surveys show that as of February 7, among the 766 preliminary survey respondents:

” 95.4% are not in favor of investing the

City’s pension fund in hedge funds.

” 82.7% believe that the pension fund should not

invest any money (i.e., a zero-percent allocation) to hedge funds,

when asked what amount Plan members might feel comfortable with

investing in hedge funds.

Clearly, 83% of Plan beneficiaries (634 of 766 respondents) are not comfortable with SFERS investing any amount of the Pension fund in hedge funds. The remaining 17% (132 of 766) who may have a higher comfort level investing in hedge funds indicated the maximum investment they would be comfortable with: 7.18% indicated 3% ($600 million), 4% indicated 5% ($1 billion), 1.8% indicated 10% ($2 billion), 1% indicated 15% ($3 billion), 0.5% indicated 25% ($5 billion), and — shockingly — 0.8% (6 respondents, 5 of which are represented by IFTPE Local 21) indicated they would Ok with a 36% allocation ($7.2 billion) to hedge funds.

In addition, the survey revealed:

When asked if Local

21’s 12- to 15-member Hedge Fund Advisory Committee should

make this decision on behalf of all 4,595 active Local 21 employees,

plus an unknown number of Local 21 retirees, only 10.6% responded

that Local 21 should make this decision for them. The remaining

89.4% percent believe Local 21 should survey all of its members

and let the membership decide for themselves.

When asked if Local

21’s 12- to 15-member Hedge Fund Advisory Committee should

make this decision on behalf of all 4,595 active Local 21 employees,

plus an unknown number of Local 21 retirees, only 10.6% responded

that Local 21 should make this decision for them. The remaining

89.4% percent believe Local 21 should survey all of its members

and let the membership decide for themselves.

So much for Local 21’s claim that only a small number of current employees and retirees are deeply concerned about how their pension funds will be invested!

It’s clear from the survey that Plan beneficiaries overwhelmingly oppose SFERS using their pension funds to invest in hedge funds. While the survey did not explicitly ask whether SFERS should be restricted from doing so in the face of member opposition, SFERS nonetheless has ethical and legal fiduciary obligations to abide with Plan beneficiary’s preferences.

It’s crystal clear that 91% of Plan beneficiaries believe that their respective bargaining unions should survey their union members to assess whether Plan members approve of investing in hedge funds, and clear that nearly 96% believe SFERS’ seven-member Board should not invest in hedge funds without first conducting a survey of all Plan members beneficiaries.

Given the preliminary

results of the on-line survey, SFERS’ Commissioners have

ethical and legal obligations to listen carefully to the preferences

of their “clients” (Plan beneficiaries), and SFERS’

Board should drop consideration of investing in hedge funds, since

the vast majority of Plan beneficiaries strongly oppose investing

their retirement fund in hedge funds.

Given the preliminary

results of the on-line survey, SFERS’ Commissioners have

ethical and legal obligations to listen carefully to the preferences

of their “clients” (Plan beneficiaries), and SFERS’

Board should drop consideration of investing in hedge funds, since

the vast majority of Plan beneficiaries strongly oppose investing

their retirement fund in hedge funds.

Wealth Transfer

Although Mayor Lee indicated in his State-of-the-City speech on January 15 that Supervisor Cohen and the Retirement Board staff have been “hard at work for months,” developing a proposal to allocate $100 million from SFERS’ Pension fund to a down payment loan program, in fact SFERS has made no decision on whether to invest Pension funds in the Mayor’s down payment loan assistance program (DLAP). The Mayor clearly reached a premature conclusion that SFERS’ Board would approve of investing Pension funds in his down payment loan program.

The Mayor claims this will help up to 1,500 families buy a first home in San Francisco, but he made no mention of “sharing prosperity” for people who are single, and the 66% of San Francisco residents who rent, and are not interested in home ownership. The Mayor may only be interested in families, not people who choose to remain single.

Indeed, in response to this author’s January 19 records request to Supervisor Malia Cohen for any and all proposals she may have presented to either SFERS’ staff or to SFERS’ Board to allocate any of SFERS portfolio toward DLAP, Cohen’s office responded on January 20 indicating that she had only made a verbal request to SFERS staff at a Retirement Board meeting last year for SFERS’ staff and the Mayor’s Office of Housing to evaluate and study a possible $50 million investment in DLAP. How the Mayor bloviated — by doubling — Cohen’s $50 million to $100 million is not yet known.

Cohen’s office

indicated that the two departments are still in the process of

reviewing and analyzing the City’s current portfolio of loans

and have not made any recommendation to either Cohen or the Retirement

Board. Once the two departments conclude their evaluation, Supervisor

Cohen will reportedly then decide whether or not to move forward

with a specific proposal to pursue an SFERS investment in DLAP.

Cohen’s office has been advised that a SFERS staff decision

may perhaps be made in February 2015.

Cohen’s office

indicated that the two departments are still in the process of

reviewing and analyzing the City’s current portfolio of loans

and have not made any recommendation to either Cohen or the Retirement

Board. Once the two departments conclude their evaluation, Supervisor

Cohen will reportedly then decide whether or not to move forward

with a specific proposal to pursue an SFERS investment in DLAP.

Cohen’s office has been advised that a SFERS staff decision

may perhaps be made in February 2015.

A separate records request on January 22 to Olson Lee, Director of the Mayor’s Office of Housing and Community (MOHCD) Development, for any correspondence between Supervisor Cohen and Olson Lee uncovered a series of 16 e-mails between Maria Benjamin, Director of Homeownership and Below Market Rate Programs in MOHCD and Bob Shaw, SFERS’ Managing Director of Public Markets. The e-mail traffic dating back to June 18, 2014 between Ms. Benjamin and Mr. Shaw is troubling.

Shaw indicated on June 18 that SFERS “will eventually need to review all of the loans that have been originated under the DALP,” but requested “a ’test’ set [of loan information] to determine what [SFERS’s staff would] need for our initial financial due diligence.” Shaw recommended looking at one specific year that was “reasonably seasoned,” and asked for DLAP loan information for 2010 because it involved “a relatively small (17) set of loans, but should provide [him] with the ability to understand the DLAP program.”

By October 17, Shaw indicated SFERS staff had completed its analysis of the sample set, and while results seemed promising, staff needed to examine the full set of loans, apparently to see if the results from the small sub-set reviewed were representative. Shaw indicated that would be critical to any proposal submitted to the Retirement Board and indicted it was too early to determine when SFERS’ staff could present an analysis to the Retirement Board, since staff still had due diligence work to complete.

Coincidentally, also

on December 3 — the same date of SFERS’ Board was presented

with three new hedge fund proposals — Ms. Benjamin submitted

additional data to Shaw, providing active and repaid loans made

since 1998 with DLAP funds. It’s not known whether Shaw has

completed an analysis of the data Benjamin provided on December

3.

Coincidentally, also

on December 3 — the same date of SFERS’ Board was presented

with three new hedge fund proposals — Ms. Benjamin submitted

additional data to Shaw, providing active and repaid loans made

since 1998 with DLAP funds. It’s not known whether Shaw has

completed an analysis of the data Benjamin provided on December

3.

But from data MoH has provided to SFERS, if SFERS’ allocates funds to the DLAP program — as the Mayor hopes SFERS’ Board will eventually do — it is very clear that investing retiree funds in down payment loans would be highly illiquid, given unknown terms of any such investments.

Whether the pension fund will involve wealth transfer to hedge fund managers, or will be tied up in illiquid down payment loans, Plan beneficiary opposition to both programs continues to grow, opposed as Plan beneficiaries are to the Mayor’s “shared prosperity” agenda using their retirement funds.

The plan beneficiaries were warned by Matt Tabbi in his September 2013 article “How Wall Street Hedge Funds Are Looting the Pension Funds of Public Workers,” that Wall Street firms are making millions in profits off of public pension funds nationwide. “Essentially it is a wealth transfer from teachers, cops and firemen to billionaire hedge funders,” Taibbi noted. “Pension funds are one of the last great, unguarded piles of money in this country, and there are going to be all sort of operators that are trying to get their hands on that money.”

It’s not just about teachers, cops, and firefighters. It’s also San Francisco employees who are nurses, librarians, secretaries, janitors, and bus drivers who rightly worry about the sticky fingers trying to gain access to their retirement fund.

When Meiberger was asked what keeps him awake at night considering his fiduciary responsibilities to Plan beneficiaries, he candidly replied:

“How would we

ever know if any SFERS investment in hedge funds is a ’success?’,”

other observers worry.

“How would we

ever know if any SFERS investment in hedge funds is a ’success?’,”

other observers worry.

On December 8, 2014 the San Francisco Chronicle posted an on-line story titled “S.F. pensions should avoid hedge funds.” It appeared the next morning in its print edition under the title “Do not hedge.” The Chronicle reported that SFERS’ overseers [SFERS’ Board of Directors] are nervous about a bold but risky idea for the city’s $20 billion retirement fund: putting a slug of money into high-flying hedge funds.”

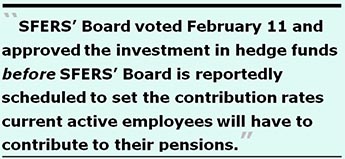

Since the conservative-leaning Chronicle is concerned about the risky “high-flying” idea and recommends against it, hopefully SFERS’ Board will play closer attention when it considers again on February 11 whether to adopt Coaker’s goofy “endowment model of investing” public retirees’ funds in hedge funds — against the beneficiary members’ substantial objections.

SFERS’ beneficiaries must act to protect their pensions, and hold SFERS’ staff and the Retirement Board members accountable in exercising their fiduciary responsibilities to prudently manage the trust fund for the exclusive benefit of Plan members and their beneficiaries.

Monette-Shaw is an open-government

accountability advocate, a patient advocate, and a member of California’s

First Amendment Coalition. He received the Society of Professional

Journalists-Northern California Chapter’s James Madison Freedom of Information Award in the Advocacy category in March 2012. Feedback: monette-shaw@westsideobserver.

Postscript

After this article

was submitted to the Westside Observer for publication, new information

surfaced.

After this article

was submitted to the Westside Observer for publication, new information

surfaced.

Comically, IFTPE Local 21 changed the name of its Hedge Fund Advisory Committee to the “Pension Advisory Committee,” perhaps to lend it more dignity. The re-named committee chaired by Gus Vallejo — who ran for election to the SFERS Board, but was beaten in the election by SFERS Commissioner Brian Stansbury — now characterizes its unanimous recommendation to SFERS to consider “responsible” investment strategies, including a “minimal investment in hedge funds.” How Local 21 can report to its membership with a straight face that “minimal” means a $2 billion investment is not known.

Not to be outdone, the San Francisco Police Officer Association’s POA Journal includes in its January 2015 edition two articles, one by Mike Hebel (a retiree who is the POA’s Welfare Officer), who wrote that that despite “consistent poor performance,” hedge funds are widely used by public and private endowments, and he supports use of hedge funds. When did “consistent poor performance” become a valid reason to invest in hedge funds?

In the same issue, the POA Journal carried a second article by Police Officer Lou Barberini from the Mission Station who opposes use of hedge funds, in part due to SFERS’ failed currency overlay program experiment pushed for by SFERS Commissioner Driscoll that invested in hedge funds and lost over $60 million in doing so.

The POA Journal carried an article in its February 2015 edition by the POA’s president, Marty Halloran, claiming facts should rule SFERS’ Board decision-making. Halloran asserts that SFERS has before it “expert advice,” from experts — ostensibly including SFERS’ expert Chief Investment Officer, Bill Coaker — who believe that placing some assets in alternative investment mechanisms is the best way to achieve some sort of balance. Halloran asserts that a Pension plan the size of SFERS’ $20 billion fund “requires a Board that can support a sophisticated investment strategy.” Is Halloran suggesting that some Board members may not be “sophisticated”?

Halloran says not

one word about the presumably sophisticated billionaires —

Buffett and Soros — who advise against investing in hedge

funds.

Halloran says not

one word about the presumably sophisticated billionaires —

Buffett and Soros — who advise against investing in hedge

funds.

Apparently Halloran and Vallejo, along with Coaker, know more about “sophisticated” investing that do Soros and Buffett.

Bloomberg Skewers Coaker’s February 11 Proposal

Speaking of Halloran’s call for fact-based evidence, despite the fact that SFERS’ Board requested on December 3 that Coaker and SFERS staff conduct due diligence on the 5% hedge fund allocation recommended in a proposal developed by SFERS Board president Victor Makras, Huish, and Coaker, a new recommendation from Coaker dated February 11 that he is presenting to SFERS’ Board continues to seek a 10% allocation to hedge funds, noting that staff would be Ok with a 5% mix, but prefers a 10% mix in order to reduce volatility of returns on investments.

He asserts a 5% allocation does not reduce the volatility of returns. Interestingly, Angeles Investment Advisors believes a 5 percent hedge fund exposure would “serve the objective of reducing volatility,” according to a new article on the Bloomberg Business web site posted on February 7.

Bloomberg’s February 7 article, however, notes:

“When

you stray from traditional structures of asset allocation into

hedge funds, you raise volatility and risk profiles,” said

David Kotok, chairman and chief investment officer of Cumberland

Advisors, a Sarasota, Florida-based investment advisory firm.

“If a pension board chases additional yield or performance

because they are in a very low interest-rate environment, then

they may be adding more risk than the anticipated additional return.”

“When

you stray from traditional structures of asset allocation into

hedge funds, you raise volatility and risk profiles,” said

David Kotok, chairman and chief investment officer of Cumberland

Advisors, a Sarasota, Florida-based investment advisory firm.

“If a pension board chases additional yield or performance

because they are in a very low interest-rate environment, then

they may be adding more risk than the anticipated additional return.”

Speaking of chasing additional “yield,” this brings us back to whether Coaker’s plan to chase alpha “excess returns” are realistic.

Coaker’s new proposal that he is presenting to SFERS’ Board, now available and dated February 11, pooh-poohs objections to investing in hedge funds raised by Plan beneficiaries and interested parties. He says that objections to investing in hedge funds raised to date “are, at best, an incomplete picture.” Coaker then claims “hedge funds have less than half the volatility of the equity market.”

What hat he’s pulling this rabbit out of is unknown. But the Bloomberg Business February 7 article noted that investing in hedge funds raises volatility and risk profiles.

Coaker’s Hookah Pipe Dream

Coaker’s Hookah Pipe Dream

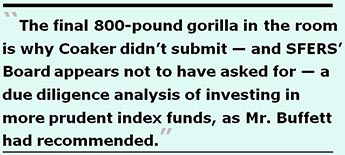

Elsewhere in Coaker’s new February 11 “due diligence” report back to SFERS’ Board, he notes that it takes time to build a high-quality portfolio, since investments can take up to 10 years before any capital is returned to the Pension fund.

Given that Coaker’s first stint at SFERS between 2005 and 2008 involved just a two-and-a-half year tenure, and his tenure at UC Regents was just six years, it’s difficult to believe that Coaker will even be around 10 years hence to evaluate how his “endowment model” and hedge fund asset allocation recommendations will have played out. As far as that goes, few of SFERS’ current Board will be around 10 years from now either, to see how things work out should they approve to invest in hedge funds.

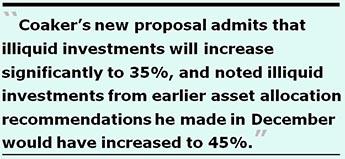

Coaker’s new proposal admits that illiquid investments will increase significantly to 35%, and noted illiquid investments from earlier asset allocation recommendations he made in December would have increased to 45%. As senior leaders in SEIU Local 1021 have noted, when you add in what SFERS is planning to invest in “alternative equities” (without calling alternative equities out as a separate asset allocation class), plus a hedge fund allocation at 15%, SFERS may be considering somewhere between 28% and 45% in risky and very illiquid investments.

Amazingly, Coaker’s

February hookah proposal claims SFERS’ staff will “conduct

onsite visits to CALSTRS (the California State Teacher’s

Retirement System), one or two other pension plans, or endowments”

to pick their brains on specified allocations to infrastructure.

But he says not one word about reaching out to CalPERS to investigate

why CalPERS had pulled out of hedge fund investments entirely.

Why would Coker do due diligence reaching out to CALSTRS, but

not with CalPERS?

Amazingly, Coaker’s

February hookah proposal claims SFERS’ staff will “conduct

onsite visits to CALSTRS (the California State Teacher’s

Retirement System), one or two other pension plans, or endowments”

to pick their brains on specified allocations to infrastructure.

But he says not one word about reaching out to CalPERS to investigate

why CalPERS had pulled out of hedge fund investments entirely.

Why would Coker do due diligence reaching out to CALSTRS, but

not with CalPERS?

Coaker’s February 11 proposal asserts that a 5% allocation to hedge funds would not reduce the volatility of returns, even though Angeles Investment Advisors asserts in the Bloomberg article that it would. Do we have disagreement here on “facts” between Coaker and SFERS’ general consultant, Angeles Investments Advisors?

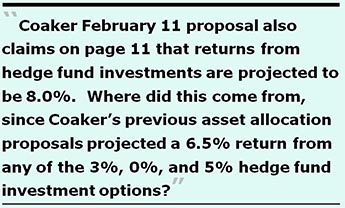

Coaker’s February 11 proposal also claims on page 11 that returns from hedge fund investments are projected to be 8.0%. Wait! What?

Where did this come from, since Coaker’s previous asset allocation proposals projected a 6.5% return from any of the 3%, 0%, and 5% hedge fund investment options? How did this mushroom from 6.5% to 8% in the two-month period between December 3 and February 11, given that Institutional Investors Alpha reported on December 29 that the London-based research firm Preqin found that two-thirds of investors seek annualized returns of 4% to 6% from hedge funds?

How on earth can SFERS’ Commissioners seriously believe Coaker knows better than Buffett and Soros, and believe he can chase alpha that even Preqin doesn’t believe will occur?

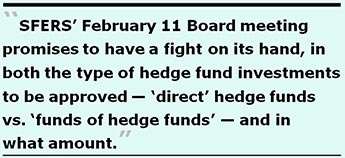

SFERS’ February

11 Board meeting promises to have a fight on its hand, in both

the amount of hedge fund investments to be approved, and which

type. Coaker’s February 11 recommendation claims that “fund-of-hedge-funds”

— purportedly preferred by SFERS’ Board but opposed

by SFERS’ staff — have fallen out of favor with “institutional

investors” for several reasons. As but one reason, Coaker

reports that institutional investors who utilize both direct hedge

funds and fund-of-hedge-funds run the risk of “over diversifying”

and “hiring too many managers in the aggregate.”

SFERS’ February

11 Board meeting promises to have a fight on its hand, in both

the amount of hedge fund investments to be approved, and which

type. Coaker’s February 11 recommendation claims that “fund-of-hedge-funds”

— purportedly preferred by SFERS’ Board but opposed

by SFERS’ staff — have fallen out of favor with “institutional

investors” for several reasons. As but one reason, Coaker

reports that institutional investors who utilize both direct hedge

funds and fund-of-hedge-funds run the risk of “over diversifying”

and “hiring too many managers in the aggregate.”

Were SFERS Plan beneficiaries interested in comedy, as opposed to fact-based information and their eventual pensions, this would be comical, were it not so sad. As it is, and noted above, the UC Regents system’s new Chief Investment Officer, Jagdeep Singh Bachler has been engaged during his nine-month tenure as CIO in a major restructuring of the equities portfolio Coaker managed at UC Regents, reducing the number of external equities managers from 70 to 40 “because of concerns that the system was paying excessive fees and owned too many securities.”