Source: San Francisco Employees’ Retirement System Annual Report Year Ended June 30, 2010, and Jeff Adachi

Article Printer-friendly PDF file

Westside Observer

October 2011 at www.WestsideObserver.com

A Giant Ponzi Scheme:

“Pension

Reform” Ballot Measures Omit Salary Reform

by Patrick Monette-Shaw

Public employees did not cause San Francisco’s pension problems.

The City’s pension problems are caused by meddling politicians, billionaires operating on the fringes of City government, and especially, the great need for City salary reform — since a minority of City employees are receiving huge salaries and pensions, while the majority of City employees receive very small pensions.

And the organizations attacking City employee pensions — the Chamber of Commerce, BOMA, and SPUR, among others — are the same guys who routinely attack City services, or alternatively keep trying to privatize City parks and other local government services.

Now they’re claiming themselves saviors of services?

Excessive management and public safety salaries that drive up excessive pensions, is one definition of a Ponzi scheme.

Another definition is safety employee salary raises calculated on cross-jurisdictional comparisons, in which salary increases in one jurisdiction drives up salaries in the comparative jurisdictions (a key provision which is enshrined in San Francisco’s contract with the Police Officer’s Association).

That’s what led Vallejo into declaring bankruptcy, though nobody admitted Bernie Maddoff would have been proud of these two Ponzi elements.

Departing from my focus on Laguna Honda Hospital, I ask that before you vote you consider various Ponzi schemes as a counterpoint to misinformation regarding San Francisco’s competing pension measures.

The dueling measures appear to have turned several of our local politicians into embarrassing panderers sucking up to billionaires — billionaires Warren Hellman, George Hume, Michael Moritz, and perhaps Larry Ellison — who claim they’re concerned about the loss of public services.

Collectively, the billionaires blame increasing City employee pension expenses on the City’s 25% cut to education, 20% cut to children’s and senior services, and 50% cut to Recreation and Parks Department, among other services.

But ostrich-like, they ignore ever-increasing management salaries, additional long-term debt voters have no control over affecting the City’s credit rating, and the City’s extraordinarily thin cash reserves — the real reasons basic services go unfunded, or are cut from the City budget. Even Moody’s downgrade of San Francisco’s credit worthiness understood this.

To borrow a line from comedian Will Durst, a polite way of saying our politicians may be beholden to certain large contributors — say billionaires — would be to say they “resemble hookers with the appetites of hippopotamuses in heat.”

Worse, Jeff Adachi and Interim Mayor Ed Lee aren’t telling San Francisco voters their dueling “pension reform” measures protect top earners while punishing over half of all City employees.

The big lie from City Hall — the same lie Adachi has pushed in the San Francisco Examiner and the Westside Observer neighborhood newspaper — is the claim that the City’s 27,000 employees average $93,000 in salaries, driving up pensions.

That’s simply untrue, on both counts. There were 36,644 City employees in 2010, including full- and part-time employees, not 27,000; the City Controller converts over 10,000 part-time employees into “full-time equivalents,” fudging the denominator.

The average salary for all 36,644 employees is $63,000, not $93,000, but there’s some caveats in the averages.

Of the 36,644 City employees in calendar year 2010, 18,972 (52%) earned less than $70,000, representing $665.7 million (25.6%) of payroll. Their average total salaries were just $35,091. In stark contrast, the 11,838 employees (32.3%) earning over $90,000 gobbled fully $1.47 billion (56.5%) of payroll. Their average total salaries were $123,874!

Skyrocketing management salaries since 2003 inflate management pensions, another Ponzi scheme. These inverted ratios disproportionately penalize 52% of lower-paid employees.

In 2003, there were 2,918 City employees earning over $90,000 in total pay, costing $314 million. In 2010, the City’s 11,838 employees earning over $90,000 is an increase of 8,920 such highly-paid employees, a staggering 305.7 percent change since calendar year 2003!

Clearly, the unfunded salary increases affect escalating management pensions — largely driven by overly-generous top salaries — which isn’t addressed in either pension ballot measure, or discussed by City officials. Neither measure reigns in top management salaries, which the billionaires ignore.

“Safety” (police, firefighters) employees recently struck another pension reform deal until 2015, announced only after Interim Mayor Lee officially entered the mayor’s race. The Board of Supervisors unanimously passed on September 13 —“without a peep” — the contract Mayor Ed Lee negotiated that will exempt police and firefighters if Adachi’s Prop. D passes.

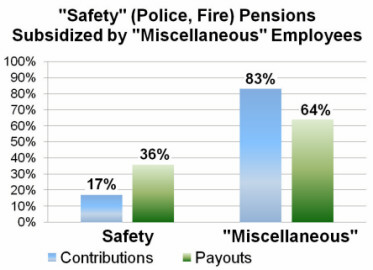

According to both Jeff Adachi and the Employee Retirement System, safety employees contribute 17% of money to the pension fund, but draw 36% of pension payouts. Non-safety “miscellaneous” employees contribute the balance, subsidizing generous “safety” pensions, an inequity unaddressed by either Prop’s. “C” or “D.”

Source: San

Francisco Employees’ Retirement System Annual Report Year

Ended June 30, 2010, and Jeff Adachi

“Miscellaneous” employees are not only subsidizing pensions of safety employees, they’re also subsidizing pay raises for safety employees and the 11,897 employees earning over $90,000 in salaries.

Billionaires Set Six-Figure CIty Pension Caps

San Francisco’s employee retirement system is healthy, solvent, well-managed, and performing well.

It earned a 12.55% investment return last year — $1.65 billion — not the 7.75% annual return Jeff Adachi’s and Mayor Ed Lee’s flawed proposals are based on. Our retirement system’s portfolio is a model for other municipalities.

But tell that to Ed Lee’s and Jeff Adachi’s billionaire backers Hellman, Hume, and Moritz.

These billionaires helped Mayor Lee’s Prop. “C” cap “safety” pensions at $183,750 and cap “miscellaneous” pensions at $208,230. The billionaires also helped Adachi’s Prop. “D” cap pensions at $140,000, even though Adachi initially claimed in last February’s Observer newspaper that his measure would cap pensions at $90,000.

The San Francisco Labor Council joined forces with San Francisco’s Chamber of Commerce, calling Prop. “C” a “spirit of shared sacrifice” ironically misnamed the “Fairness Float,” since wholly unfair.

While they urge you to Vote “Yes,” here’s why you might consider voting “No” on “C” and “D”:

The City’s payroll data shows fully half (50%) of the City’s 36,644 employees earned a $65,000 average salary, or less. Over one-third (37%) of City employees average salaries of less than $45,000.

Those at the lowest end of City salaries can least afford a 6% pension contribution increase on top of the 7.5% they are already paying, nor can City retirees afford health care increases who may be forced into dropping dependent coverage for minor children or elderly parents, if either Prop.’s “C” or “D” passes.

Prop. C’s proposed pension increases discriminates against the City’s lower-paid current employees, requiring a flat 10% pension contribution for those earning $50,000 to $100,000, rather than using a sliding scale. For instance, the 3,579 employees who earned between $50,000 and $60,000 will pay the same 10% pension contribution as the 2,333 employees who earned between $90,000 and $100,000.

Prop “D” uses a sliding scale, but employees earning below $70,000 may pay up to 13% of their salaries towards pensions, while those earning $100,000 to $200,000 pay only15.5%. Adachi’s sliding scale has five $10,000 ranges for those earning $50,000 to $100,000, each $10,000-step increasing an additional half a percent, but only three $50,000 ranges for those earning over $100,000. Each $50,000-step increases only half a percent, which is patently unfair to low-wage earners.

Current employees may face paying 16% to 20% of their wages towards pensions and health care, plus additional unknown health care co-pay increases, if either “C” or “D” passes.

Fixed-income retirees will also see their health care costs soar, and will lose their supplemental COLA, which retiree’s (but not current City employees) are only paid when retirement fund investments yield a surplus.

Similarly, while the City’s pension system data shows 1,218 retirees (6.1%) earned pensions more than $100,000, 41% (8,143 retirees) earned pensions less than $25,000, 32% (6,369 retirees) earned pensions less than $20,000, and 22.5% (4,480 retirees) — nearly one quarter — earned pensions less than $15,000.

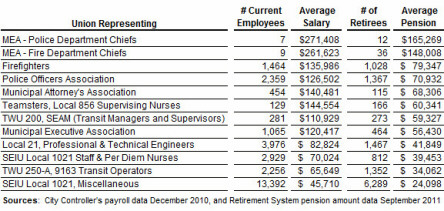

Service pensions average $79,347 for firefighters; $70,932 for police officers; and $27,623 for “miscellaneous” employees (inflated by $100,000+ salaries of “some miscellaneous” staff).

Employees earning $60,000 with 13 years of service at age 62 earn small $18,000 pensions. Highly-paid managers and safety employees earning over $100,000 continue collecting six-figure pensions.

The “shared sacrifice” is a myth. Top wage earners and top retiree’s share little sacrifice!

Scapegoating Public Employees

Public employees didn’t cause the national economic recession, and shouldn’t be ”goated for it, here or nationally.

The San Francisco Weekly published an article by reporter Joe Eskenazi on August 31, in which he claims the defeat of Jeff Adachi’s pension reform measure “Prop. B” in November 2010 led to a “direct result” that Moody’s lowered the City’s credit rating from Aa1 to Aa2. Eskenazi blames the credit rating downgrade only on defeat of Prop. B, which is patently untrue!

By omission Eskenazi doesn’t tell the full story, since Moody’s cited numerous reasons, including in its report that the credit downgrade:

Then there’s the $1.47 billion in skyrocketing salaries noted above. This totals $5.4 billion in unfunded obligations, between management salaries and long-term debt that City employees didn’t create — that neither Prop. “C” nor Prop. “D” addresses, and which the billionaires ignore.

The City’s lowest-paid employees shouldn’t be ”goated for the Moody’s credit rating downgrade.

Adachi’s Desperate Misinformation

In a San Francisco Chronicle article on May 12, Adachi claims only half of City employees contribute toward their pensions; he claimed the City picks up 100% of pension costs for about 10,000 employees and [11] elected officials. That’s now untrue: In July 2011, at least 13,392 of the lowest-paid employees represented by SEIU began paying 7.5% of wages towards pensions.

He claimed on May 12 the Mayor’s proposed Prop. C would use pension “smoothing” over a ten-year period rather than over five years. The Mayor’s final proposal does not utilize pension smoothing.

Adachi claimed increased pension costs consume nearly half of our City’s deficit, and that his measure would save $400 million over five years, or $80 million annually. But he mentions nothing about the $100 million the City just approved in long-term COP debt for the Mascone Convention facilities (which will further affect the City’s credit rating), or the $20 million tax break for Twitter.

He’s now saying his pension reform measure will save $1.6 billion over ten years — or $144 million annually — without explaining why he claimed just months earlier savings of only $400 million over five years, or $80 million annually.

Adachi claimed in May that if the pension fund didn’t achieve it’s assumed 7.75% annual rate of return, San Francisco’s pension “crisis” will worsen. But he completely ignored data that shows the pension fund earned a 12.55% return in the year ending June 2010. Between Adachi’s Prop. “B” in 2010 and his Prop. “D” in 2011, he continues playing lose and fast with accurate data.

In his May 12 San Francisco Examiner article, billionaire Warren Hellman stated “The notion that the City’s pension fund is in immediate meltdown is simply not true.”

We’re not in meltdown mode, and the Ponzi scheme must be addressed. Until salary reform occurs first, there can never be meaningful pension reform.

Adachi has noted the backroom deal Mayor Ed Lee crafted for safety employees will cost taxpayers $127 million over the long term, and that wage and benefit reductions for City employees will be frozen until 2013, potentially only for firefighters and police. This portends “miscellaneous” employees who earn the lowest salaries and pensions may face further wage and benefit reductions — to subsidize those at the top — if either Prop.’s “C” or “D” passes.

Voters have an ethical obligation, and the right, to reject both measures. Billionaires who bill themselves as champions of City services have no guarantee services will be improved from pension reform, nor do the rest of us.

Vote “No” on both “C”

and “D!”

Monette-Shaw is an open-government accountability advocate, a patient advocate, a member of California’s First Amendment Coalition, and a write-in candidate for Mayor. Feedback: monette-shaw@westsideobserver.com.

Top

_______

Copyright (c) 2011 by Committee to Save LHH. All rights

reserved. This work may not be reposted anywhere on the

Web, or reprinted in any print media, without express written

permission. E-mail the Committee

to Save LHH.